Is a rebound in cereal and oilseed prices on the cards?

CRM analyst Benjamin Bodart told us since November last, feed compounders, speculators and investors have been watching climatic developments for telltale signs of production volumes and future prices.

“We can’t be bearish about the cereals or maize market currently with uncertainties lingering over weather patterns in South America,” said the analyst.

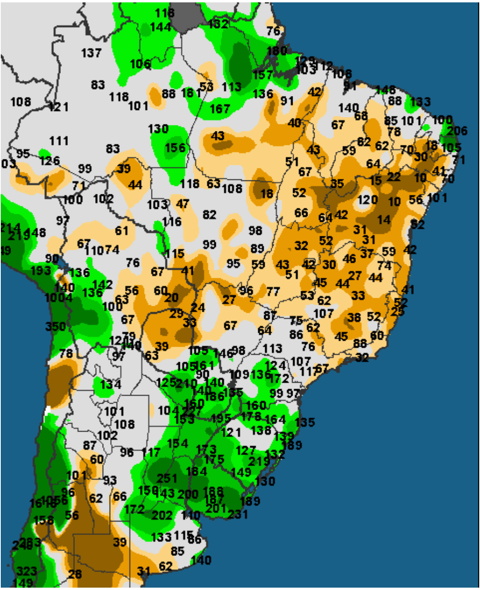

He said in the weeks up to the end of December, the North and South part of Argentina were very dry. “While conditions in the center, the core maize/soy production region, remain conducive to a good harvest, temperatures in the range of 35 to 40 degrees Celsius are forecast for the next ten days in the northern part of Argentina, not good news for cereal production there,” said Bodart.

The northern and eastern regions of Brazil are also relatively dry, and though rains are forecast for those areas, the total precipitation recorded over the past few weeks has been low. “The maize and, as a result, wheat market could be supported if those factors lead to a reduction in the South American harvest levels,” said Bodart.

Soybean meal prices

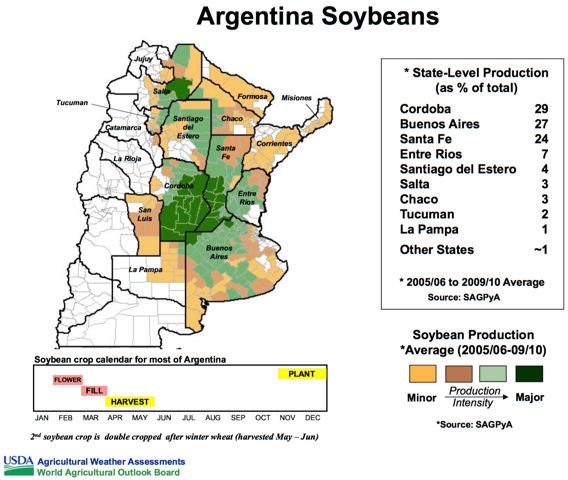

He said it is evidently too early to make a call on Brazilian soybean production, a country which has been forecast to produce 103 to 106 million tons of soybeans in this year’s harvest – if realized, a record, or in Argentina, the leading soybean meal exporter globally. “If we keep seeing high temperatures and a lack of precipitation, and thus a reduction in output in those countries, there could be a rebound in soybean and meal prices,” said the market watcher.

Moreover, he said the strength of the dollar against the euro and sterling, on the back of the pending Trump presidency, could make it more expensive for European based feed compounders to import soybean/soybean meal from the US.

But as banks and private investors are also predicting parity in the euro and the US dollar, Bodart said it is a case of wait and see. “Currency effects will likely play a huge role in the [agri-commodities market] in 2017,” he added.

In terms of wheat, the analyst said there was also some winter kill risks apparent with a huge drop in temperatures over the past few weeks in the Black Sea production region but also across the US Plains– in Kansas and Nebraska – coupled with little snow cover. “We can’t put a figure on winter kill just yet but 2017 US winter wheat output could be lower as a result, particularly given the fact there was the lowest planted area there for decades,” he said.

The prices of wheat and maize in the US are historically low at the moment, continued Bodart.

“And if investors buy up wheat, offering support to US prices, such a move could also lend support to the European wheat market, given the CBOT Wheat is the global benchmark market for that cereal,” explained the analyst.

However, he reckons we might soon be seeing the end of the long bearish period on cereal and oilseed prices globally. But it will take more though than just those weather related concerns to cement such a pricing trend, he acknowledged.