Rabobank: Strong US meat exports, Japanese and South Korean beef imports on the rise

They noted that US meat exports have been strong in response, despite the headwinds of trade policy uncertainties. US beef prices have held up well despite production growth, added the analysts.

The pork complex is the main driver behind expanding total protein supplies in the US, according to the publication. Year-to-date production is up 4% with a 4% to 5% increase also expected in 2019. US poultry production has been up 2.5% in 2018 and price pressure and negative returns to processors in that segment are expected to hold expansion in check next year, despite new processing facilities coming on stream. The increased production in the US requires it to boost exports across all proteins, said Rabobank.

Though the Rabobank team noted US prices in the first half of 2018 have held up remarkably well given the production levels, they said that increased supplies of total proteins and potential trade fallouts are emerging concerns. Indeed, increased beef supplies and trade uncertainty look set to impact US prices in 2H 2018, said the beef market specialists.

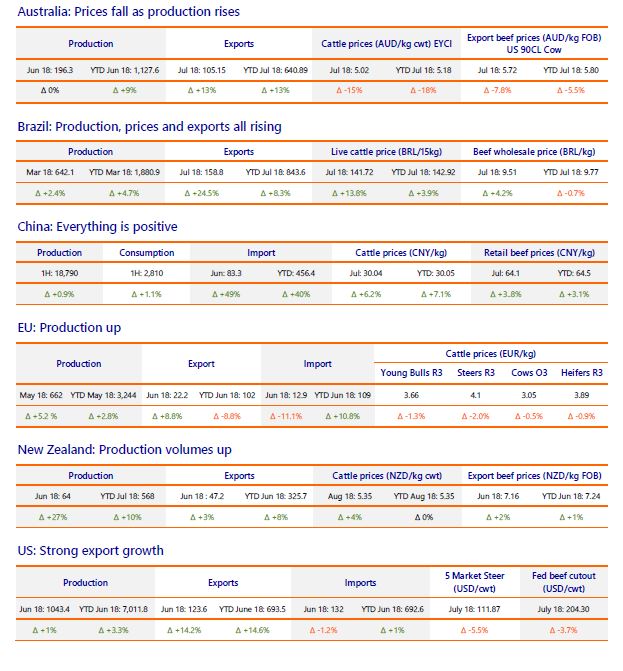

Brazilian beef exports

Strong export markets and the normal seasonal decline in cattle supply are providing the foundations for improved cattle prices in Brazil in Q3 2018. Brazilian beef exports have rebounded. China, the second largest buyer of Brazilian beef, increased its imports by 44% in the first eight months of this year.

Rabobank thinks Brazilian beef exports will finish up 5% higher in volume terms compared to 2017 levels by the end of 2018.

Asian outlook

Japan and South Korea beef imports are on the rise, continued the quarterly report.

In 2017, combined imports by Japan and South Korea were up 9%, and at their highest level since 2002. Along with improved economies and lower global beef prices, the availability of beef from Australia and the US is fueling this growth. Australian exports to Japan and South Korea are up 11% for the YTD (June), while the US appears to be focusing more on South Korea, with exports up 41% while up only 6% to Japan.

Japan has also granted access for Argentina to export fresh beef into the country for the first time with the first shipment, albeit small, arriving in July. This decision would be a positive indication for Brazil who is also entertaining the prospect of gaining access to Japan.

At the start of 2018, Rabobank reported on growing competition and complexity in global markets, and the opportunities and pressures this could bring to margins along beef supply chains.

“Part way through the year we have seen corporate results reflecting this mix of challenge and opportunity. Some global beef companies have revised down their earnings expectations, due to a combination of trade disruptions and ample protein supplies, while others have credited beef with contributing to high earnings. On balance, we see more margin pressure looming.”

African Swine Fever

Several outbreaks of African Swine Fever (ASF) were recorded in China in recent months, which raises the possibility of China – the world’s largest consumer of pork – being caught short, said the Rabobank team.

“While the extent and timing of any herd liquidation remain uncertain, if ASF takes hold, it is likely that China will increase imports of pork – and other meats such as beef – in 2019. An associated lift in global pork prices could also benefit beef supply chains in other regions.”

EU production is up

The Rabobank analysts reported that drought is having a major impact on the EU beef complex, with higher slaughter numbers recorded across large parts of Northern Europe - Northern Germany, Denmark, Sweden, Poland and Ireland. Feed prices are expected to continue rising, reducing producer margins and leading to additional cattle liquidation, in particular in older animals and young stock.

The team said higher slaughter numbers will cause the cattle inventory to continue to fall in Europe, although they added that an improving milk price may support dairy cow retention and offset some of this fall in the coming months. With continuing dry conditions, EU beef supply is expected to remain high in the coming months.

EU beef exports fell 4% for the first five months of 2018 compared to the previous year. Turkey became the most important market, with volumes doubling in that timeframe. Turkey now represents 15.5% of the total EU beef export.

Rabobank said that China offers opportunities for European beef, with Ireland, France and other countries recently receiving export approval.