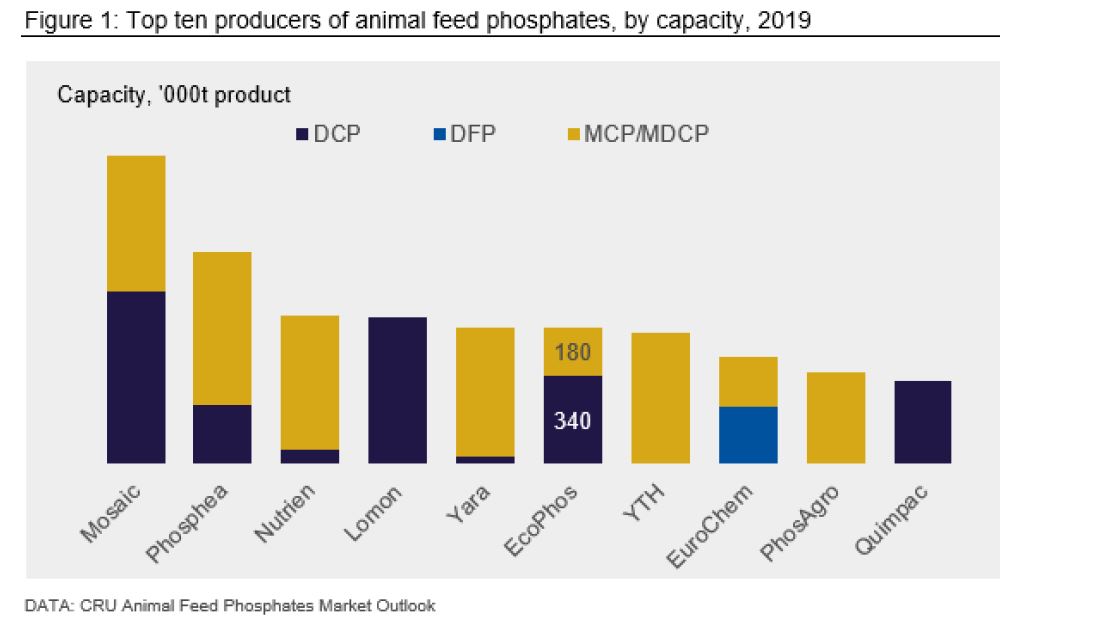

Capacity consolidation dominant trend in the feed phosphates market

2019, in particular, was a difficult one for the broader phosphates market in terms of prices, said Chris Lawson, research manager, fertilizers, CRU.

“The downstream fertilizer prices were hit by a perfect storm of poor demand in places like the US and China and new capacity coming on stream in Morocco and Saudi Arabiaa; lower fertilizer prices translated through to lower phosphoric acid prices, and that led to lower prices for feed phosphates, which were also undermined by the reduced demand in China due to the ASF outbreak there.”

In terms of the reasons behind the slight turnaround seen this year, Lawson said prices got to such a low point in 2019 that there was some idling of capacity in China, which was followed by the Covid-19 lockdown in that market, a factor that added to tightening supply there. Those developments have been followed by a terrific upswing in demand for fertilizers, a trend that has been very supportive of prices, said the phosphate market specialist.

"So, essentially, we have had a rebalancing of the supply and demand dynamic, and higher prices across the board this year.”

Capacity consolidation

Regardless of that rebound, the industry has been suffering with very stagnant demand and, as a result, there are very few new capacity projects being commissioned this year or the next, he said.

“With the low-price environment having been the big story of the market for the past few years, we have seen some capacity consolidation and that has helped to tighten up the market. Yara has closed its feed phosphates manufacturing plant in Helsingborg, Sweden, but the bigger story was Aliphos, which was part of Ecophos, going bankrupt in March.”

No company to date has taken over the Aliphos’ assets, he said.

Ecophos cited a steep decline in phosphate product prices since 2016, along with competition from new players with cheaper production costs as the key reasons for the bankruptcy filing. It had acquired the Aliphos feed phosphates business from the Tessenderlo Group in 2013.

The closure came as little surprise to the industry given the issues the company had faced with successfully commissioning projects, its shrinking share in the weak animal feed market, and its exposure to imported raw material prices, said the analyst.

“However, the Aliphos bankruptcy remains the single biggest development in the feed phosphates arena this year, and the industry is still trying to realign itself now that capacity is missing. If you look at overall capacity, that producer was the seventh largest globally, so it is a fair chunk that has been taken out of the market.

“But there is signficant oversupply; the amount of capacity far exceeds the amount of demand there is for feed phosphates, so just because Aliphos has gone bankrupt, we don’t necessarily think that is going to tighten the market significantly and cause a big wave of new investments, new capacity, but it will, at least, help to correct the supply and demand balance,” said the CRU analyst.

Will that be enough to avoid other bankruptcies in the sector in the future?

“There is still going to be pressure on those high cost marginal producers, on some of those small-scale producers who are not integrated with their raw materials. But this development should partially alleviate some of that pressure.”

Demand dynamics

CRU had been anticipating demand growth in China this year but the analysts believe any increase in that market will be relatively modest.

“We don’t have significant figures on that just yet, but we know that the size of the swine herd there is starting to increase again and that has helped to trigger the buying of basic feed commodities such as corn and soybean meal. We do see some demand rebound there.”

Some of the surrounding Southeast Asian countries might prove the brighter spot in terms of future feed phosphate uptake, he said.

Brazil is another strong market, as is Latin America, in general. “Brazilian agricultural has been performing outstandingly well this year. The devaluation of Brazilian real has helped to increase the margins and profitability of a number of agricultural producers there this year.”

Global demand has been shifting away from dicalcium phosphate (DCP) towards monocalcium phosphate (MCP), he added. “DCP’s share in the market will continue to shrink.”

Asked whether phytase use in feed formulations is still a threat to feed phosphate market growth, Lawson said it was more of a threat in developing markets where phytase does not have significant penetration.