Russia-Ukraine conflict escalates already high-cost situation for milk producers

In addition, milk producers around the globe are facing higher corn and soybean prices for the next two years, finds Rabobank in its Global Dairy Quarterly Q1 2022.

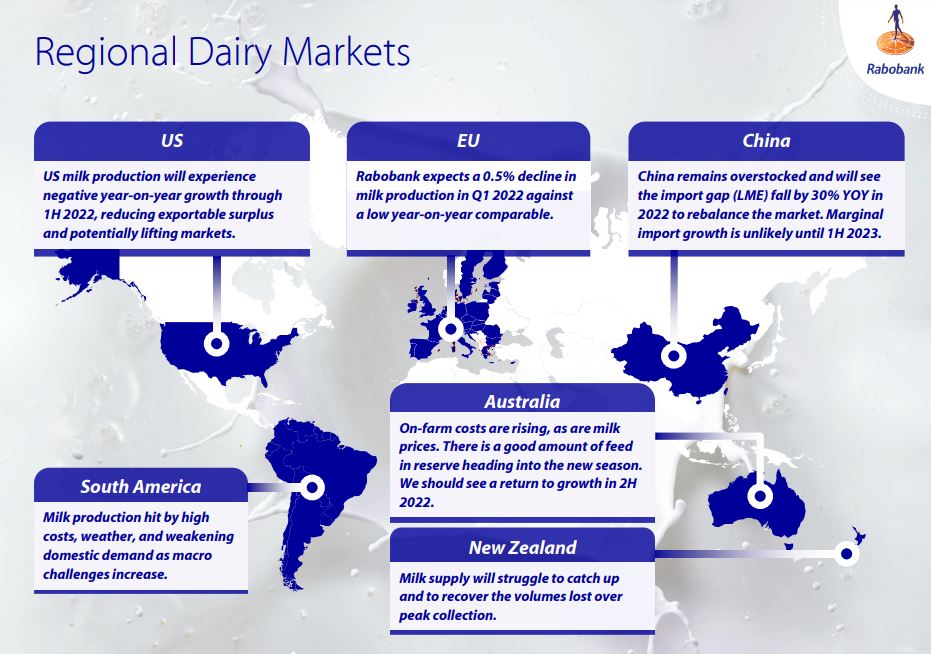

Persistently unfavorable weather in the southern hemisphere, high and rising production costs, and lingering disruptions from COVID-19 will lead to a year-on-year decline in milk production in the Big-7 exporting regions in the first half of this year, against 1H 2021’s high comparable, forecasts the dairy market specialists.

The team expects a mild recovery in the second half of 2022.

In response to the supply-side shortfall, dairy exports will slow this year, they added. China’s import requirement is expected to trend much lower in 2022 due to ample domestic stocks and continued production growth, commented the analysts.

“Based on Rabobank’s supply and demand forecasts, exports in liquid milk equivalents are expected to decline year-on-year through 2022, a duration not previously experienced,” said Sandy Chen, senior analyst, dairy, at Rabobank.

Feed costs

With feed costs flying north, there is little hope for meaningful relief through 2023, said the Rabobank team.

Drought is sharply reducing South America’s soybean and corn production. High input costs and uncertainty about agrichemical supply are putting downward pressure on yields and acreage expectations.

The situation is further exacerbated by the Russia-Ukraine conflict, which could impact ports and supplies from Ukraine.

Together, Russia and Ukraine account for 28% of global wheat exports, 18% of corn, and 30% of barley. Additionally, Russia supplies about 40% of Europe’s natural gas. Global commodity markets are already tight as regions battle drought, rising fertilizer costs, and falling yields and acreage.

"Russia's invasion of Ukraine presents significant upside price risks for energy, fertilizer, and agricultural commodities, which will have a spillover impact on feed costs, feed availability, and ultimately on dairy commodity prices and farmgate milk prices."

Moreover, with inflation running rampant worldwide – and increasingly felt by consumers – there is a high likelihood of inflation persisting or staying elevated over a longer period. This will influence consumer behavior and invite hawkish monetary policies, reads the report.

Structural changes in Europe

Northwest Europe is facing a structural decline in milk supply, finds the publication.

Lower 2021 annual milk production in France, Germany and the Netherlands reflects the heightened national oversight on farmed animal production, noted the analysts.

The government in the Netherlands is proposing a 30% reduction in the dairy herd by 2030 to lower nitrogen emissions. Belgium is following the same route as the Dutch authorities, and France and Denmark have set out new GHG emission targets.

Germany is also seeing an increasing focus on animal welfare and labelling proposals attached to that.

Fit for 55, the EU's target of reducing net greenhouse gas emissions by at least 55% by 2030, Farm to Fork, the EU Green Deal, combined with the new CAP, will become overarching guidelines for agricultural policy at the EU and at national level, said Rabobank.

Such policies could "structurally" add extra costs to the value chain, and put pressure on milk volumes, especially in NW Europe, where livestock production is dense, stressed the analysts.