Special Edition: Aqua feed innovation

Rabobank sees role for feed industry as the driver of change in aquaculture

“At this point then, the feed capacity growth is lower than the farming growth, especially looking at it from the stance of the non-vertically integrated producer, from the perspective of the independent, specialized feed players,” Gorjan Nikolik, senior analyst, seafood, RaboResearch, told us.

He has written a report in reaction to these developments outlining the opportunities for the fish feed industry in such a scenario - How to Succeed in Aqua Feed: The Feed Industry Should Be the Driver of Change in Aquaculture. The target audience for his study is the investment community, along with fish feed manufacturers and fish farming companies.

Nikolik believes aqua feed companies can respond to the maturing fish-farming industry by combining feed with a range of complementary inputs, such as genetics, animal health products, data analysis solutions, hardware, and farm management software, in order to extract previously unobtainable synergies.

“This is a menu of options. Not all of this is possible for all feed companies, not all those ideas will work for all companies. But there are many technologies adjacent to aqua feed – we should see aqua feed companies in the center of the value chain – they have a lot of competence in terms of really understanding the ingredients and production, and they have access to the farmers.

“If they begin to see themselves as more than just an aqua feed company, if they see themselves as an aqua technology company or an aqua venture capital investor, taking those two ideas and building a more diversified group could be a way of creating a lot of value, and, at the same, time increasing growth and driving the aquaculture industry, even driving sustainability in the sector.”

It was the feed companies that drove aquaculture development at the onset of the industry, that brought in the technology, that educated new entrants, that created change, he stressed.

“Based on that logic, we can now see aquaculture feed companies doing more in a number of ways. They can further embrace digitalization, data, sensors and hardware, which are complementary products to the feed, allowing for greater feed efficiency, and they would be selling to the same customer. There is also the biological aspect, they can combine genetics, feed and vaccines. Only recently have genetics and animal health products become so sophisticated that they can be tailored to the local environment and to the feed for a desired effect.”

He acknowledged that there is already a move in this direction by some fish feed players. His report can further guide those companies along that route but also inspire others as they embrace such change. The research is also valuable for potential investors in the sector, said Nikolik.

Fish farming trends and impact on feed sector

Looking at the trends in farmed fish production and the impact on the global feed industry, the analyst said the salmon, freshwater and shrimp sectors all have challenges, but the obstacles differ depending on each of those segments.

“In the salmon industry, there is maturity, there is consolidation and vertical integration, while in the freshwater species sector, there is a change in demand driver, and there is need for companies to look for growth in other parts of the world with a different model, so that has its own challenges,” he said.

In shrimp, there has been sector volatility induced from biological challenges, a trend that led to oversupply in feed capacity in markets not affected by disease, particularly in India, added the analyst. “Growth is coming back to the shrimp farming sector, but there is probably no requirement right now to build new feed mills.”

Salmon

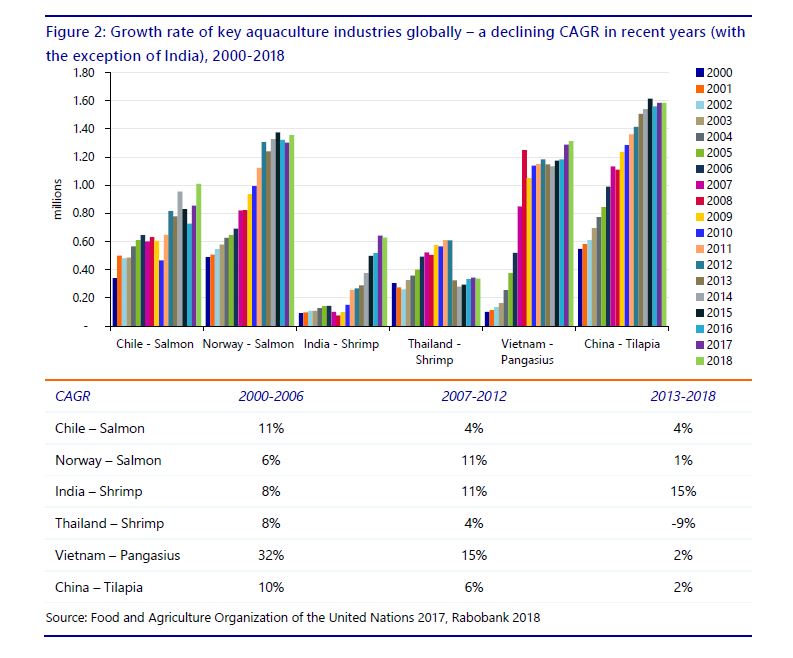

Digging deeper into salmon farming trends, Nikolik said Norway is seeing very limited growth, while Chile has been faring slightly better. Due to legislative limits and biological challenges, salmon production, overall, will not see the growth levels like in previous years, when it was reaching between 6 and 7%. Nevertheless, the sector should see growth rates of between 2 and 5% in the coming years.

“But, for feed players, it will be less than that, because a large part of the growth has been eroded by the vertical integration trend. Granted, the biggest part of that has happened already within the salmon sector – with Mowi and Bakkaforst – but there is still a risk that something may happen, in this same regard, in Chile.

"We can say that the general profit pool in salmon feed has declined, there is stagnation.”

Shrimp

There was a huge amount of hype about the market potential for shrimp production in India. The investment boom in India accelerated after 2013, and continued up until 2018, he said.

“In 2011, the vannamei shrimp sector took off and it really grew 20-30% per year, rising to 650K/700K metric tons in terms of output in 2018. A giant industry was born in a really short period of time. Indeed, in early 2018, there were still broker reports forecasting that 1m tons would be reached by the sector in the next one-two years. It was growth rate extrapolation, and feed companies there were building factories - they might have started building them in 2016 or 2017 and were finishing off construction, doubling their capacity, but then there was a price crash in 2018, followed by another one in 2019 [due to large inventories created above demand growth].

“So it soon became clear that India was not going to grow at the forecast level. We saw that the industry contracted in the first half of 2019. Maybe, we will have a small recovery in the second half of this year, but I don’t know if it will be enough to make up for the loss of volume in H1 2019.

So there is close to zero growth for India. “All the extra feed capacity created is obviously not going to be used. It will take years for India to get back to the growth curve needed to spur further investment in feed capacity there.”

As so often happens in agricultural commodities, he continued, a few years of rapid expansion is followed by oversupply and price crashes. “People get over optimistic and think the growth trend is going to last forever, so there is overproduction.”

Thailand, which used to be the number one shrimp producer globally but was devastated by EMS and never fully recovered, has large feed overcapacity as well, said the analyst.

“Everyone is betting on Ecuador. I think it is only a matter of time when the feed capacity exceeds demand there as well.

“Nevertheless, Ecuador is currently doing well. It saw 20% growth this year. Ecuador is, in fact, supplying a completely different market – China - than India, which supplies the US, and when the prices crashed globally, it seems Ecuador’s market was less affected.”

Ecuador ships product that is minimally processed to the Chinese, compared to India which dominates the peeled shrimp segment. “Chinese demand is strong, and its own shrimp production is weak. But the question remains how long can Ecuador continue to grow at this pace.”

Freshwater fish

In terms of the freshwater species, tilapia and pangasius, fillets had long been the driver of the farmed freshwater fish sector, with China and Vietnam dominating in the frozen fillet market. For years, the frozen fillet segment had seen double-digit growth rates driven by Western markets demand. In addition, the feed industry for these species expanded to eventual reach 10m metric tons globally.

However, there has been a contraction of those sales, considerably so in Europe after a defamatory documentary in Germany on the Vietnamese pangasius. There have also been trade restrictions imposed by the US market such as anti-dumping measures on pangasius exports and tariffs imposed on tilapia products from China due to the ongoing trade dispute between Washington and Beijing, said Nikolik.

The result, he said, is a freshwater aquaculture industry with considerable oversupply, falling prices, and a lower profit pool for the entire global value chain, including feed production.

Chinese producers of tilapia have thus been shifting away from the US and moving towards their own domestic market. “But let’s see how long that can last because the US really imported a lot. Let’s see how much China can consume. But the point for the Chinese and the Asian [producers of farmed freshwater species] is that they need to find growth somewhere else. But the question is whether some of these players are big enough to move to new markets. I think some of them have ambitions to be global players, to set up in Latin American and in African markets.”