USDA: US feed crop producers to see dwindling global market share though 2028

The US Department of Agriculture (USDA) released data on anticipated US feed crop production and trade through 2028/29 in a new report on Friday [November 1]. To generate the analysis, it was assumed that US-China trade tension would remain through to the end of the decade.

The analysis highlighted the increasing importance that the international market plays for US feed crop producers, the report authors said. “The US has been a major supplier of many commodities in global markets for decades,” they added.

As domestic yields increased for crops like soybeans, corn and wheat, US crops have been competitive by reducing production costs, they said. But domestic demand for food products mostly relies on population growth to drive demand.

“Depending on the commodity, this means that US producers are relying more and more on global outlets to market the crops they produce,” they said. “As a consequence, international markets play a larger role in how US producers fare.”

During the 2018/19 marketing year, US producers exported about 37% of the soybean crop, 15% of corn and 50% of the wheat crop, the authors said.

“However, foreign competition continues to strengthen, and even though export volumes are likely to remain steady or grow, the United States is expected to continue to lose global market share across a variety of commodities.

“Producers in different regions across the world can leverage their advantages, often in terms of lower land costs, such as in Brazil, or in lower transportation costs and closer proximity to importing markets, as with Black Sea grain exporters,” they said.

Looking forward, the long-term price prospect is mixed with some initial gains fading by 2024, they noted.

“Soybean and wheat prices are expected to increase initially through 2022/23 and 2023/24, respectively,” they said. “Thereafter, soybean prices slowly decline to the 2016/17 level, while wheat prices fall to the 2017/18 level and remain there through the projection period.”

“Corn prices follow a similar pattern but are expected to fall back to 2014/15 levels by the end of the projection period,” they added.

Considering corn

Until 2011/12, the US was the dominant exporter of corn internationally, the report authors said. At that time, the US provided more than half of all exports, by autumn 2018 exports accounted for about 39%.

That market share is forecast to drop to about 36% by 2028/29, they said.

In 2018, about 38% of corn was used in ethanol, about 37% went for livestock feed and 16% of the crop was exported, they said. Going forward, feed and residual use of corn is expected to see about 20% growth through 2028/29 as meat production and consumption increases.

Although there was a bump in prices, they are expected to decline to $3.70 a bushel by 2026/27, they said.

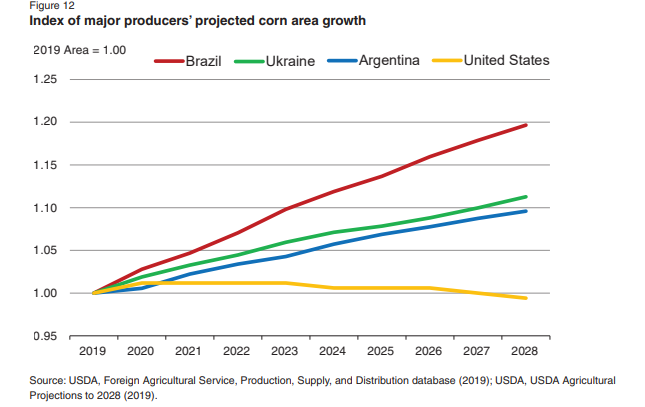

“Before the beginning of this century, the United States accounted for around 70% of world corn exports (and about a third of globally traded wheat) and was an undeniable pricemaker for both commodities,” the authors said. “The emergence of new low-cost producers and exporters in the global corn and wheat markets have reduced the US share of grain exports and transformed global grain trade. Competition from Brazil, Argentina, and Ukraine are driving down the US corn export share.”

Currently, the US is the top corn producer and exporter, but as corn output and exports from Brazil, Argentina and Ukraine increase, the US position will fade, they said. By 2028/29 those Brazil, Argentina and Ukraine are expected to export more than half the corn trade globally.

However, the US is expected to remain the top exporter of feed corn to Mexico – which is forecast to see a 30% growth in feed use by 2028/29, they said. “Almost all the increase in projected US corn exports is to come from the augmented shipments to Mexico.”

In Southeast Asia, increased production is set to grow imports mostly from Brazil and Argentina, and countries in North Africa and the Middle East are also expected to turn to South American corn producers or Ukraine.

“South and Central American corn-importing countries, such as Colombia, Chile, and Guatemala, are expected to increase corn feed use (for beef, pork, and poultry) and imports by almost 30% over the next decade,” the authors said. “Argentina and Brazil have preferential trade terms with other MERCOSUR countries, including Colombia and Chile, so they are preferred trading partners.”

Wheat market highlights

US wheat supplies about 10-15% of global demand, the report authors said. However, the market share has fallen from about 20-30% coverage before 2010.

Both prices and returns for wheat are anticipated to fall as wheat planting decreases in favor of other crops, they said.

“Over the projection period, aggregate US wheat production is expected to grow very slightly, largely based on modest gains in yields,” they forecast. “Gains in yields offset a general trend toward reduced planted and harvested acreage.”

Following 2023/24 wheat acres are predicted to fall as returns drop, they said. Global competition in the wheat market from the EU, Russia and Ukraine presents a headwind.

“Exports through 2028/29 are essentially level as the U.S. continues to serve established partners and to act as a residual supplier to the balance of the wheat importing countries,” the authors said. “Limited growth in utilization more than offsets tepid growth in supplies through 2028/19, resulting in a steadily tighter all-wheat balance sheet.”

Soybean predictions

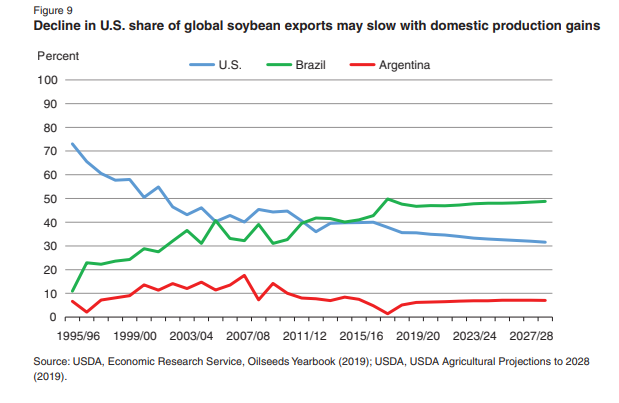

US soybean exports started facing competition from Brazil in the 1990s. The country continues to increase its soybean production and has been taking steps to address delivery challenges including paving transit routes and expanding rail services.

Argentina – the third-largest soybean exports – remains a competitor for global market share, they wrote.

“This competition was expected to continue, reducing the share of US soybeans in international trade to about 31% by the end of the projection period,” they added.

Domestic demand for the feed ingredient is expected increase and soybean crush is anticipated to increase, they said. The domestic market provides 75-80% of the demand for soybean meal.

However, as soybean production recovers in Argentina, demand for US soybean meal exports is expected to slow, the authors said.

“The Argentine share of global soybean meal exports is projected to remain steady around 45.5%,” they said. “In contrast, a receding market share for US soybean meal exports will continue through 2028/29 as slow production gains were expected to be mostly absorbed within the domestic market.”

The US share of the soybean meal export market is set to drop from 18% in 2019/20 to 16% by 2028/29, they said.

Keeping the current share of the global export market for soybeans faces challenges from international competition, they said. “Until those barriers to exports to China are lifted or reduced, US soybean trade will be more focused on the rest of the world,” they added.

However, international demand for soybeans will continue to be led by China, the authors said. “Through 2028/29, the importing countries other than China are projected to account for only 23% of the gains in global soybean imports.”