Slowdown in pork production forecast but better feed prices

Despite facing significant challenges, the analysts note that consumption remains resilient.

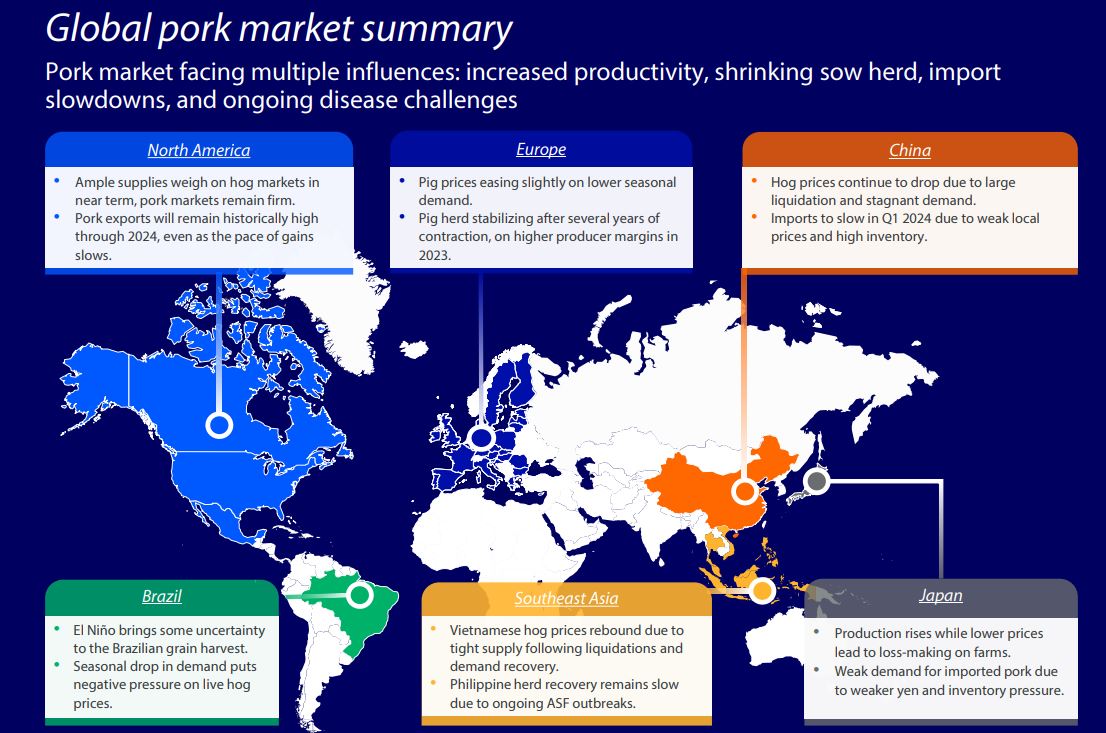

The contraction in the sow herd is expected to result in a decline or flat production in China, the US, and some European countries throughout 2024, with disease pressures adding to the industry's challenges.

While some regions grapple with declining herds, others like Brazil are on the rise, driven by global demand. Rabobank underscores the uneven growth across the globe, with African Swine Fever (ASF) outbreaks and loss-making pressures accelerating breeding herd reductions in Asia, particularly China.

Chenjun Pan, senior analyst of animal protein at Rabobank, cautions that disease outbreaks may contribute to ongoing uncertainty in 2024. Despite these challenges, she predicts continued productivity improvement driven by genetic advancements, enhanced farm management practices, and cost reduction strategies.

Feed prices

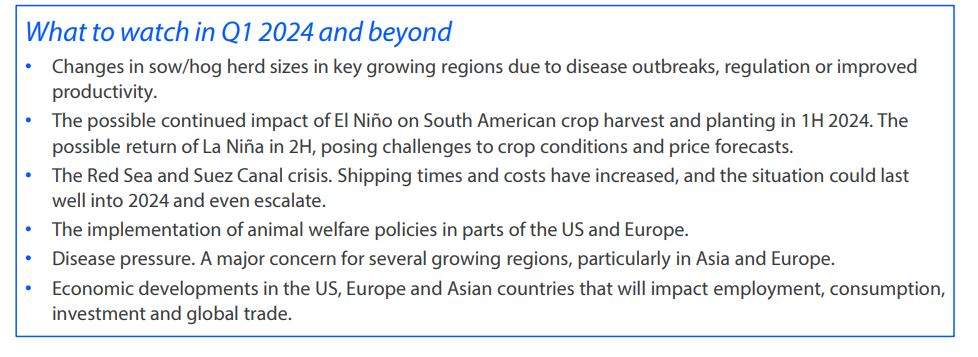

A glimmer of hope arises from decreasing feed prices, with corn and soybean prices down 15% to 25% over the past year. However, the report emphasizes that weather-related volatility could still impact feed supply and pricing dynamics.

Consumer spending on pork in key regions provides further optimism for the industry. As inflationary pressures ease and some regions experience economic rebounds, the outlook for pork consumption remains positive.

Rabobank's forecast suggests a potential contraction in global pork trade during the first half of the year, primarily due to high inventories in importing countries suppressing demand.

Pan anticipates a soft market for pork exports, particularly considering the ongoing crisis in the Red Sea and Suez Canal, hindering European shipments to Asia.