Outlook for animal protein consumption is positive

In 2018, global beef production is predicted expand for a third consecutive year, and global pork production is expected to see another year of significant expansion. Poultry production is also expected to grow, but will be down slightly on 2017, according to RaboResearch’s Animal Protein Outlook for 2018, released today.

Alternative proteins, though, will grow further from their small base and continue to capture consumer interest in innovative food, said Rabobank.

“It is not the total size but the high growth rates that alternative protein products are witnessing that commands so much attention.”

Aquaculture

In seafood, aquaculture continues to drive seafood supply growth.

“The salmon market is recovering, fishmeal prices will stabilize, and the shrimp industry is likely to continue growing.”

Aquaculture is expected to continue to grow next year, albeit at a gradually declining rate. Rabobank estimated growth in both 2017 and 2018 to be in the range of 3% to 4% in volume terms.

“Despite good growth persistent risks such as disease issues, trade policies and weather problems continue, especially in Asia, which is the most important producer of farmed seafood,” cautioned the researchers.

An expected stagnation of production in China, the largest producer, is more than offset by new growth regions, especially in South East Asia, Latin America and Africa. India is an example of a rapidly growing export orientated aquaculture industry that has been doing very well in 2017, said the authors.

The bank also expects the wild catch industry to recover after El Niño recedes in 2017.

Novel proteins in feed

The animal protein production chain, and especially aquaculture, will focus on alternative proteins as an innovative feed ingredient, forecast the report.

“Bacterial and insect based proteins show the highest potential as alternatives to fishmeal, while algal oil is considered a potential alternative to fish oil. We expect 20 to 30% of the non-vegetable source of oil to come from algae sources in the long term.”

“Antibiotic growth promoters (AGPs) are due to be removed from animal feed in Indonesia and Vietnam in 2018. In Indonesia, the ban applies to all feed, but in Vietnam, it does not apply to starter feed or to disease treatment, which will come into effect in 2021. AGP removal will likely cause higher mortality rates in open house broiler farms.”

Trade

Rabobank said its trade scorecard for 2018 shows that many countries are looking to increase exports.

“Trade should be the top-of-mind issue for global animal protein as we head into a new year, and enhancing competitiveness is going to be critical for success.”

Uncertainty in 2018 will come from the heavy overlay of politics in trade policy such as the NAFTA negotiation, Brexit and the US-China trade relationship as well as biosecurity issues such as Avian Influenza (AI) , African Swine Fever (ASF) and Enterocytozoon hepatopenaei (EHP) in shrimp.

Technology driven innovation

When it comes to innovation, technology, and in particular data-driven technology, is starting to deliver value along the animal supply chain for instance by increased supply chain cost management. “Two important drivers behind the increase of technology are reducing the environmental footprint and addressing social concerns.”

“The EU poultry industry has gone through a few turbulent years, with more than 1,000 cases of AI. Despite this, the industry is still performing well, amid well-balanced supply thanks to ongoing strong demand and flexibility in export market.

“The industry will keep growing by at least 2% in 2018, supporting further expansion in Eastern Europe, while Western European countries focus on concepts.”

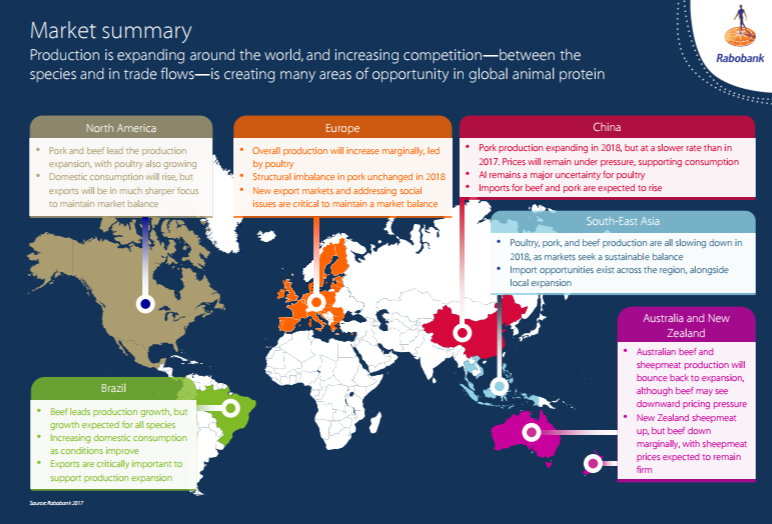

Regional outlooks

- North America: Production continues to grow. Ongoing production expansion across the species increases the dependence on trade, yet access to trade markets will be an area of uncertainty during 2018

- Brazil: Production will increase in 2018. Brazil and Argentina are set to increase beef production by 5% and 4%, respectively, with Brazil also expanding poultry and pork production.

- EU: Exports are key in a challenging market. Access to export markets is increasingly important for processors, as production rises, while social issues remain top of mind for domestic consumers.

- China: Pork supply will increase, poultry will stay flat. China’s pork market is entering a down cycle, with imports set to rise as structural adjustment continues. Overall poultry supply will be flat, with white bird supply declining and other species rising. Beef supply will grow steadily, with imports being the main driving force.

- South-East Asia: Production growth will decelerate. Poultry production is tapering off in response to oversupply. Beef demand will continue to be met by imports, with price being the main focus in trade decision making.

- Australia and New Zealand: Beef and lamb production will remain steady. Improved seasonal conditions support Australian producer demand for cattle amid softer export markets, while in New Zealand, beef exporters are reliant on continued demand growth in export markets.text-ad