Feed additive tracker: Focus on lysine, methionine and vitamin prices

Other feed additives under significant selling pressure are vitamin A, inositol – but it was coming down from record-high levels – and vitamin C pure, according to the latest outlook from Kemiex.

For vitamin A, a rather unstable and complex product to manufacture, market participants are wondering if prices have hit rock-bottom, or if there is still room for them to fall further, Stefan Schmidinger, head of markets and strategy, Kemiex, told this publication.

China’s vitamin A export levels to Germany rebounded in June, with similar demand hikes seen for such shipments into Denmark, Mexico, and UK, as per the data readout.

Kemiex also saw an interesting import surge in Brazil for vitamin E from China, along with continuing robustness in terms of sales of the vitamin into the Netherlands, but German demand for that product weakened in June, following what had been six months of significant flows.

Interestingly, European producers have reportedly been offering better terms on vitamin B5 prices than the two main Chinese suppliers, said the trading and procurement specialists.

Returning to amino acid price trends and Evonik announced today that it is increasing MetAMINO prices by US$0.35/kg in Latin America following a similar move in China three weeks ago.

A few days ago, a fire broke out at the CJ CheilJedang methionine plant in Kerteh, Malaysia, which was extinguished by more than 60 firefighters within hours. The company is currently conducting inspections to investigate equipment damage and the cause of the fire, but, as of yet, it has not issued any force majeure notifications. In previous years, CJ has exported around 130 to 150 k tons per annum.

Vitamin A production

On the capacity side, BASF, as we reported earlier this month, announced that it will be expanding its vitamin A formulation plant in Ludwigshafen, with a mid-2023 start-up planned. That follows its vitamin A acetate upgrade in 2021 to a nameplate capacity of 3,800 tons yearly.

And DSM announced a technological breakthrough this month, one that enables it to conduct market tests of the first bio-based vitamin A, beginning in its cosmetics division.

China’s Garden Biotech also recently announced progress in terms of its planned 6,000 tons per annum vitamin A facility; it has expansion projects planned for other products as well, namely a 20,000 t/a vitamin E 50% plant, a 5,000 t/a vitamin B6 (3’000 t/a feed grade) site and 200 t/a Biotin (60 t/a pure, 7’000 t/a feed 2%) unit.

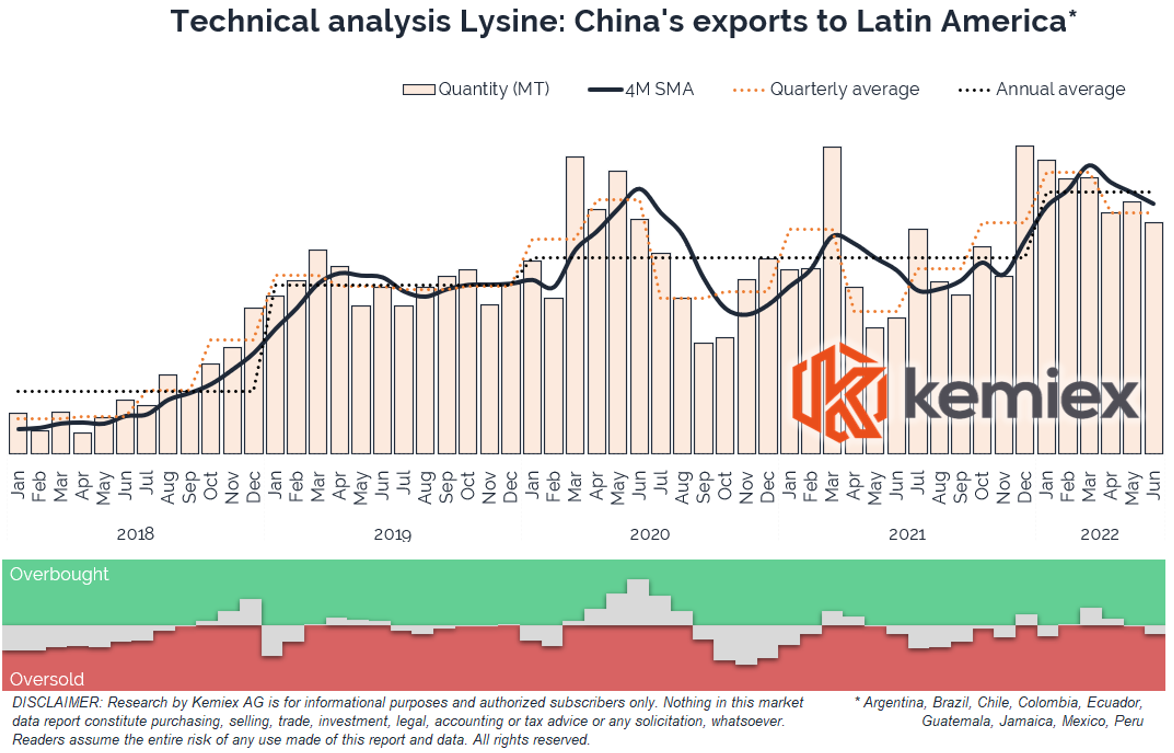

Lysine trade flows

To ensure sufficient supply of certain agricultural and industrial products, the EU recently set updated import tariff quotas. For lysine, the quota for H2 2022 was recently set at 122,500 tons, of which about 80,000 tons remain, according to the Swiss firm’s market outlook.

For threonine, the full-year quota of 166,000 tons shows a balance of about 43,100 tons for the remainder of the year.

Kemiex has also been reviewing global lysine trade flows, with it noting that the EU has imported less of that amino acid from China and Indonesia so far in 2022, with Korea benefiting.

In the first half of 2022, lysine exports from China to the world hit a record 530,000 tons, added the Zurich-based company.

Logistics challenges

Catching up on ongoing transport challenges and Kemiex noted that global supply chains are under pressure due to threatened strikes, as per the averted railroad worker action in the US earlier in July, and actual stoppage occurring in various regions.

In North Europe, German dockworkers dismissed employer offers and carried out a two-day strike earlier this month at the country’s North Sea ports. In Peru, last week, truckers started an indefinite strike to protest about the rise in fuel prices and the breach of government agreements. In June, roadblocks and country-wide demonstrations hindered transport in Ecuador and Panama, and high congestion levels, yard density and low labor availability are keeping harbor productivity low in most European ports.

Meanwhile, freight rates continue to soften or stay flat and single containers from China are available within a comfortable two weeks’ notice. However, costs remain at a multiple of pre-COVID-19 levels, said the Kemiex spokesperson.