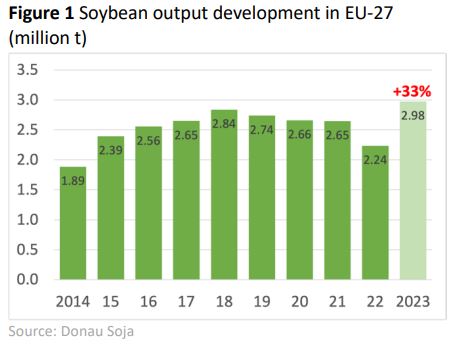

EU soy output to hit record high

“While a large part of Europe suffered again from dry and hot weather in the summer, most of the drought-affected regions were outside of the key soy producing areas,” notes a new market report published by the European non-GMO industry association (ENGA), in close cooperation with Donau Soja and ProTerra.

That publication summarizes the major trends and developments affecting non-GM soy, corn and rapeseed supply and demand dynamics within the EU.

The team estimates that the EU soybean area will be 1.1m ha in 2023, only a marginal change from last year, and they expect soybean yield in the EU to reach 2.73 t/ha, 3% higher versus the 5-year average. MARS, the EU crop forecasting service, anticipates a similar enough yield.

Soy tonnage in the wider European region is forecast at 12.2m tons, found the latest Donau Soja market report. The European harvest volume increased by almost a quarter compared to the previous year. The largest increases were recorded in Ukraine, with a rise of almost 1m tons, up 20%, to 4.8m tons. Two-thirds of European soy production take place outside the EU, mostly in the Ukraine and the European part of Russia.

Price trends

EU non-GM soy prices have declined over the past three months. “In late October, non-GM soybeans were traded at €410/t at the Bologna Exchange, a benchmark price for the EU. This price level is 20% lower when compared to the €500/t recorded in August.”

Non-GM soymeal premiums in the EU have remained relatively stable and at historic low levels over the past six months.

“Abundant imports from Brazil and Ukraine as well as low demand for non-GM soy put pressure on the premiums throughout the 2022-23 season. Most recently, the record European crop weighed on the premiums. However, the premium for HP non-GM soymeal in Northern Germany leaped to €70/ton in October despite relatively stable premiums in other regions of the EU. The explanation for the higher premiums in the North Sea ports lies in their greater distance from the typical European soy production areas. European Non-GM soy raw materials, especially Ukrainian products, are currently struggling to reach the North Sea/Baltic ports such as Brake or Rotterdam.”

The authors predict that, in the short-term, the record crop in the EU and the wider region is likely to contribute to greater availability of local non-GM soybeans, and additional pressure on premiums.

Demand dynamics

They also envisage non-GM soy demand in Europe remaining stable, due to greater availability of local beans, the low non-GM soymeal premiums making non-GM feeding programs more attractive along with the increasing demand for regional and deforestation-free raw materials in Europe, in addition to new processing capacities at ADM’s non-GM soy crushing plant in Mainz, Germany.

No grain shortages ahead

The authors do not anticipate any shortages to emerge in the supply of non-GM feed grain in the EU throughout the 2023-24 season. The recovery of the EU corn crop and Ukraine’s export potential ensure that corn demand in the EU is covered.

Corn output in the EU-27 is forecast to expand to 59.9m tons in 2023, up 12.7% compared to 2022.

And key watch points in the global corn market for the coming weeks are the planting progress in South America and geopolitical developments in the Black Sea region. “No big price swings are likely if South American plantings proceed normally.”

Drop in rapeseed acreage on the horizon

Rapeseed output in the EU-27 is estimated at 19.8m tons in 2023, up 1% from last year’s harvest. “Harvest was finished in August. The sowing of winter rapeseed started in the EU in October. A slight drop is likely in the acreage for the 2024 harvest.”

The Euronext rapeseed price has continued to drop, reported the authors, with it moving to €421/tons at the end of October. “The global market looks well supplied for the 2023/24 season, which puts downward pressure on prices.”

In the EU-27, only non-GM rapeseed is produced. But import is needed to supply the demand within the bloc, with a percentage of that likely to be GM.

According to a EC forecast, the EU-27 will import 5.8m tons of rapeseed in the 2023/24 marketing year, 1m tons less than that estimated for 2022-23.

The main source of EU rapeseed imports is Ukraine, accounting for roughly 40% of the EU import volumes in that raw material. While there is no legitimate commercial production of GM crops in Ukraine, the USDA maintains that 10-12% of its rapeseed production is GM.

Canada and Australia also play an important role in supplying rapeseed to the EU. Both countries have GM rapeseed varieties in commercial production. In 2022, the share of GM varieties in the total rapeseed area was estimated at 95% in Canada and 25% in Australia.